-

What We DoWith our integrated fleet services, you get the entire fleet management and leasing market from a single source and can purchase, finance, manage and sell your fleet cost-effectively. And you only ever pay for what you actually use.Overview

-

ResourcesWe have a lot to share. Browse our resources library for current insights, data, strategies, and success stories from our own experts in their respective fields.Overview

-

About UsWhen Holman was founded in 1924, we set something positive in motion. Our consistent focus on people and our commitment to integrity make us who we are today.Overview

Join Our TeamWe’re not just in the automotive business, we’re in the people business. Join us for the ride.Browse Careers

Join Our TeamWe’re not just in the automotive business, we’re in the people business. Join us for the ride.Browse Careers

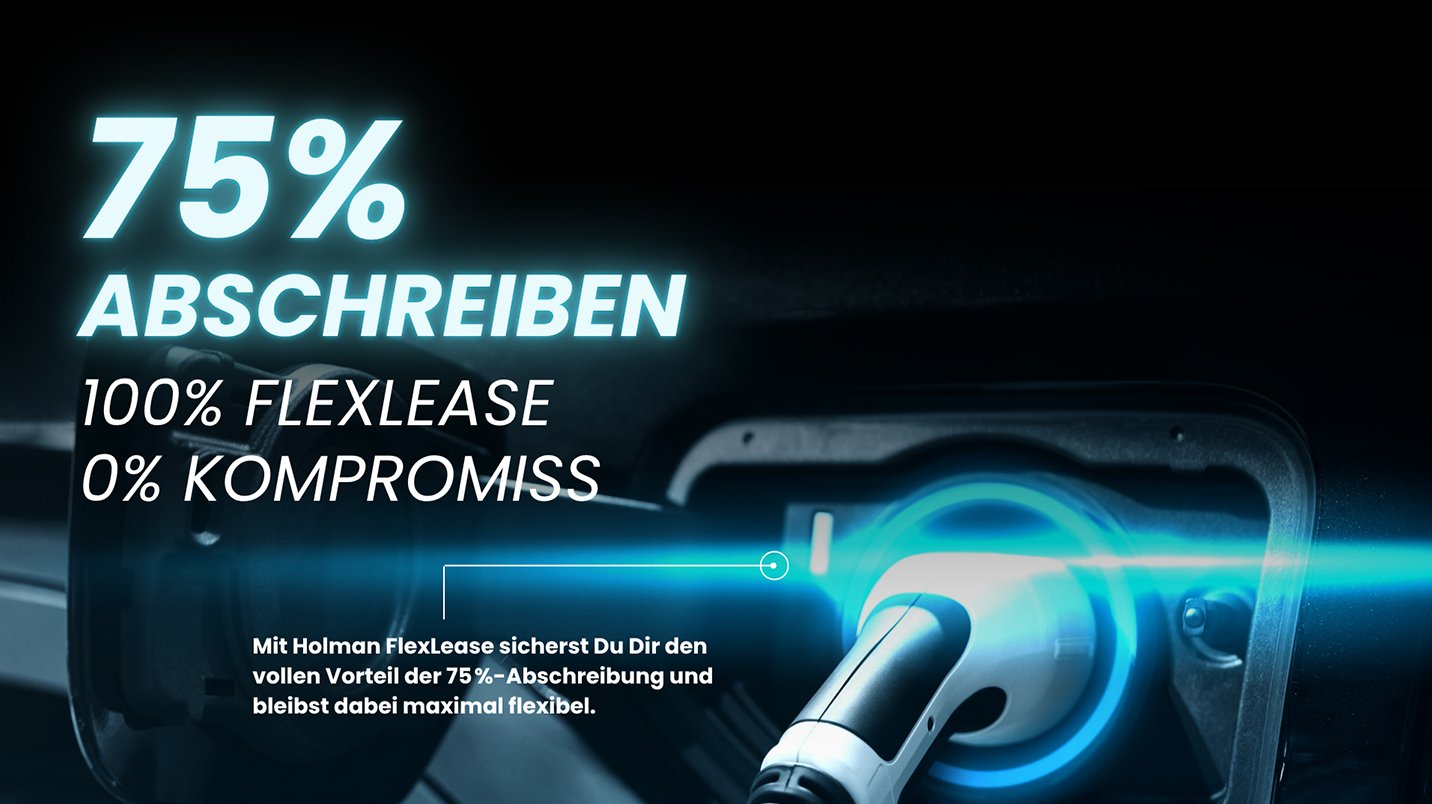

75% Special Depreciation: How to Avoid the Leasing Trap

It was the hot topic in the fleet industry this summer: With “an investment booster for e-mobility in companies,” the German government aimed to promote company-used electric vehicles through accelerated depreciation of 75% of the purchase cost of electric vehicles already in the year of investment. Sounds fantastic! Immediately write off 75% of e-vehicles – who could possibly object?

Headwinds from the Market

Instead of the expected cheers, the government faced a wave of disappointment. The Deutsche Automobil Treuhand (DAT) describes it as a support measure that “misses the target group in practice.” The reason: those who lease e-cars do not benefit from the special depreciation. But leasing is the predominant form of financing in the commercial sector. The trade media eurotransport.de expressed a similar view: “What at first glance looks like a real investment booster turns out to be hardly usable for many fleets – especially if they rely on leasing.”

Let’s do a reality check

Is that true? Do fleet managers automatically fall into a trap when leasing an e-vehicle? The answer is: it depends. They do fall into the leasing trap if a traditional closed-end lease is agreed upon. In this model, the vehicle remains on the lessor’s balance sheet. The result: you can neither claim regular depreciation (AfA) nor the special depreciation for tax purposes.

But there is a strategic alternative: With Holman FlexLease, we offer an innovative open-end leasing model that picks up where traditional leasing ends: you, as the lessee, become the economic owner of the vehicles. The result: you can fully claim the 75% special depreciation (and the regular AfA) for tax purposes.

How much does depreciation bring: Sample calculation

Is the switch worthwhile? How much tax benefit does Holman FlexLease actually provide? In the following overview, our experts show a direct comparison of the tax effect between traditional closed-end leasing and Holman FlexLease in the first year (assuming a tax rate of 29%).

Example: Škoda Enyaq

Vehicle price: €25,196.63

Lease term: 3 years

Monthly lease payments: €375.26

Savings in the first year: €5,480 in taxes

Savings compared to closed-end leasing: €4,175

Our answer to whether switching to Holman FlexLease is worthwhile is: yes. The tax savings for the Škoda Enyaq amount to nearly 17% in the first year. Every fleet manager can calculate that with ten or more vehicles, this represents a significant liquidity advantage. We would be happy to calculate the specific opportunity for your fleet in a direct consultation.

Have questions?

Now is the perfect time to restructure your fleet.

Get non-binding advice and secure your tax advantages!

Deutsche Automobil Treuhand GmbH. (2025, Juni 5). Voraussichtlich eher Placebo als Booster. https://www.dat.de/news/voraussichtlich-eher-placebo-als-booster/

Holzer, N., & Nolle, G. (2025, Juli 15). 75 %-Sonderabschreibung: Leasing geht leer aus. eurotransport.de. https://www.eurotransport.de/logistik/verkehrspolitik/sonderabschreibung-e-pkw-leichte-nutzfahrzeuge-busse-und-lkw-2025-leasing-kein-vorteil/

Presse- und Informationsamt der Bundesregierung. (2025, Juli 21). Wachstumsbooster zur Stärkung des Standorts Deutschland. https://www.bundesregierung.de/breg-de/aktuelles/wachstumsbooster-2351752

Next Post

Timing It Right When Selling VehiclesRelated Resources

Explore more related industry news, insights, and developments.